Municipal bond investors are beginning to price in a wildfire premium for local government borrowers they perceive as facing greater risk of loss.

“I do think this year will prove to be a bit of a turning point for some climate risk pricing signals in the market,” said Erica Smoll of Breckenridge Capital Advisors at last week’s Brookings Institution Annual Municipal Finance Conference.

Smoll was responding to research presented at the meeting showing that investors are now charging materially higher yields to districts facing greater future fire risk.

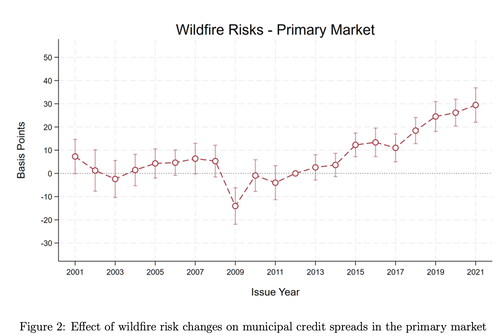

According to research by Woongchan Jeon from the Center of Economic Research at ETH Zurich, by combining detailed weather forecasts, land use information, and data on U.S. municipal bond spreads, U.S. municipalities projected to face higher wildfire risk already pay more to borrow.

Specifically, the research finds that a one standard deviation increase in anticipated wildfire exposure is associated with a 14 basis point rise in primary market spreads and a 26 basis point rise in secondary market spreads—exceeding 40% of the average spread in the sample.

The report adds that these effects are stronger in communities with larger minority populations and greater dependence on local revenue.

“Starting from 2015, the spread started to diverge,” Jeon said. “And one standard deviation rise in wildfire risks is associated…with the 14 and 26 basis points rise in primary and secondary market spreads after 2014.”

The research combined physical wildfire potential with the exposure of housing units in the Wildland–Urban Interface to create an “economic wildfire risk” metric for municipal school districts, then mapped that risk onto each bond’s maturity.

Because school district debt is backed by property taxes, localized climate shocks directly threaten repayment capacity.

Crucially, the research design exploits differences within the same issuer—longer-dated bonds embody more of the mid-century wildfire risk trajectory than near-term maturities. This allows the researchers to difference out fundamentals and isolate the effect of changing risk expectations.

The team also probed pricing mechanisms.

"Starting from twenty fifteen, the median housing values started to decline a little bit,” Jeon noted, tying forward-looking residential behavior to credit pricing.

Distributional impacts surfaced as well: districts with larger non‑white populations and those more reliant on local revenue bear larger spread penalties, even after controlling for income.

This raises the specter of a “vicious cycle,” where higher borrowing costs shrink fiscal space, undercut recovery and public goods provision, and in turn worsen credit conditions.

Investors’ New Worries: FEMA, Insurance, and Mega-Fires

Smoll linked the market shift to policy and insurance shocks, not just climate awareness.

She pointed to “rhetoric coming out of the executive branch about potential changes to FEMA or outright dismantling of that,” which is altering how managers view federal backstops.

At the same time, “we’ve now had a few years in a row of these really large increases in property insurance premium… And you’re actually starting to see some weakness now in housing prices.”

The January 2025 Los Angeles wildfires provided a stark case study: widely held Los Angeles Department of Water and Power bonds “very often traded prior to the wildfires—it was trading twenty basis points…” before spreads widened in the aftermath.

Jeon suggested that new policy innovations and adaptation measures may be needed to address the wildfire pricing trajectory.

“If we can design some adaptation bonds that can help these districts to adapt to future climate risks, then maybe we might be able to help them out finance their public project,” he said.