- ■ Life reinsurance will never be the same

- ■ No magic model fix for California's wildfire market

- ■ APAC corporate physical risk multiplies

PE, Hedge Fund Scramble Has Permanently “Rewired” $5 Trillion Life Reinsurance Market

Researchers from Harvard Business School report that annuity transactions have fueled 90% of the asset growth at major alternative investment firms in recent years while fundamentally transforming the global life reinsurance industry.

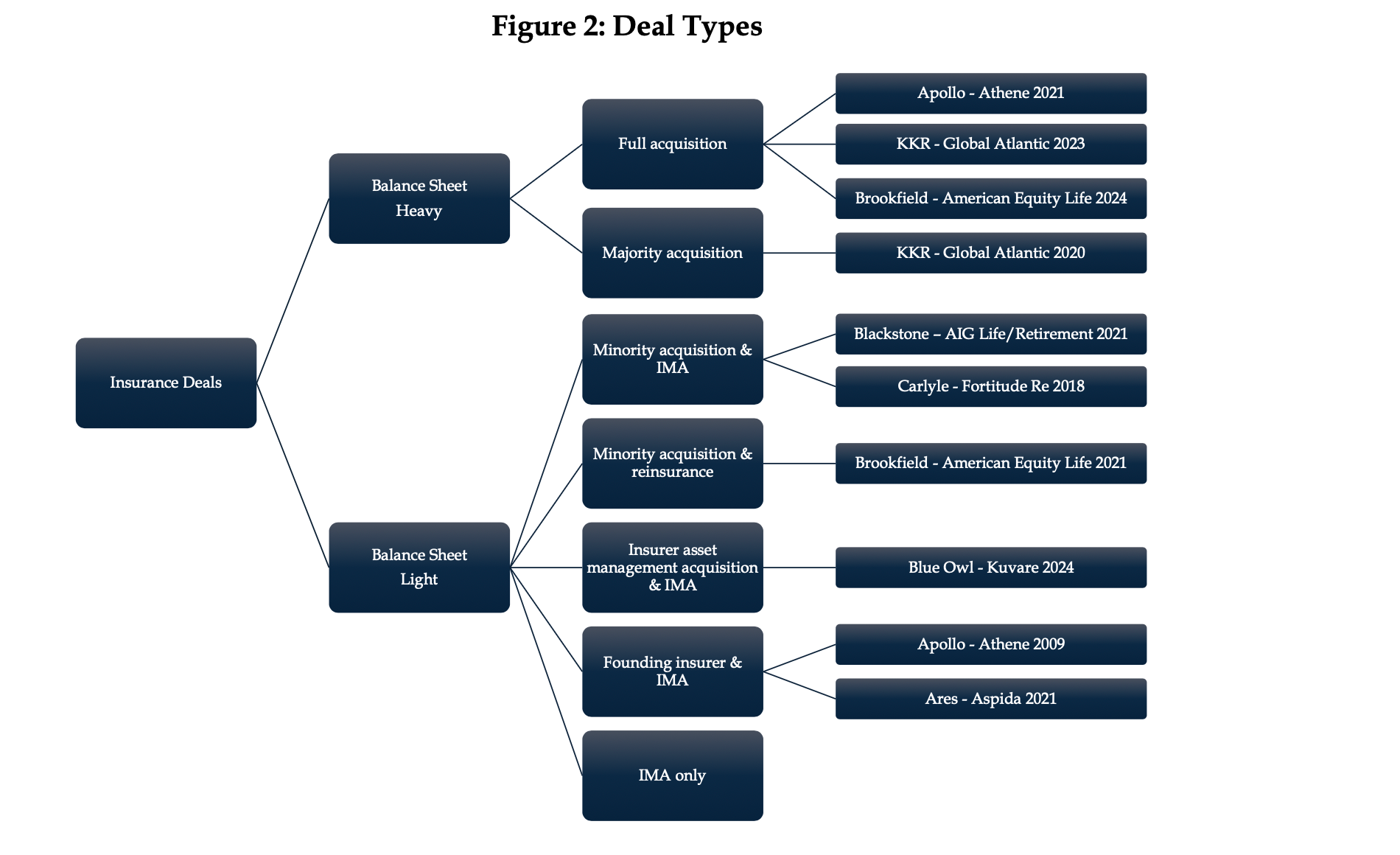

The insurance deals pursued by alternative asset managers represent more than opportunistic deal-making, but constitute a foundational re-platforming of the entire industry that is reshaping competitive dynamics, investment strategies, and long-term value creation across financial services.

The study, from Harvard State Street Associates, analyzed a decade of data from major publicly listed alternative asset managers (AAMs) controlling $5.5 trillion in assets, revealing that alternative asset firms with insurance partnerships now account for 90% of total industry assets under management (AUM), up from just 15% in 2014 and that the integration insurance and alternatives has become the dominant growth strategy, not a short-term trend.

Transformation Is Structural, Not Tactical

"Our findings suggest that insurance partnerships are not a peripheral trend, but a foundational re-platforming of the alternative-asset-management industry," the paper release last week says. "As AAMs rewire their capital base around annuity float and reinsurance flows, they reshape not only their own balance sheets and earnings but also the contours of competition, investment product design, and long-term value creation across financial services."

The data reveals striking patterns: Apollo's AUM grew by more than $250 billion in the three years following its merger with Athene, with credit strategies accounting for $200 billion of that growth. Similarly, Blackstone's insurance deals drove year-over-year AUM growth of approximately $260 billion, while Ares saw $300 billion in AUM growth following the founding of its insurance platform Aspida.

From Episodic to Permanent Capital

The research identifies how insurance partnerships fundamentally alter the alternative business model by replacing episodic, closed-end fund structures with continuous streams of permanent capital.

"Life insurers, by contrast, collect policyholder premiums continuously; fixed and fixed-indexed annuities alone generated roughly $280 billion of new deposits in the United States during 2024," the study notes.

This shift from transient to permanent capital has enabled explosive growth in credit strategies, which increased nearly tenfold from 2014 to 2024, reaching $2.5 trillion. Insurance-heavy AAMs now hold a disproportionate share of credit AUM compared to their equity holdings, reflecting how captive insurance float provides stable demand for newly originated loans and private placements.

The authors lay out in stark language the economic value of each alternative-backed annuity deal that has flooded the market over the past several years.

"Each block acquisition or reinsurance treaty can add tens of billions of incremental AUM, immediately raising management fees or spread income," the report says "For example, Blackstone’s 2021 transaction with Allstate Life transferred $28 billion of assets at closing and secured a long-term mandate for additional run-off portfolios, boosting Blackstone’s fee-earning AUM. Insurance float therefore restores a scalable growth vector at a time when traditional LP capital appears demand-constrained."

Revenue Mix Fundamentally Altered

The transformation extends beyond asset growth to reshape revenue composition of life reinsurers.

For insurance-heavy AAMs, spread income from insurance operations now represents the majority of revenues, though fee income still accounts for approximately 50% of earnings due to higher margins, researchers say. This diversification has reduced earnings volatility, with spread-based income providing greater stability than performance fees.

However, the benefits come with trade-offs. Insurance-heavy AAMs exhibit lower return on equity and receive lower valuation multiples; trading at price-to-earnings ratios approximately 5-10 points below their asset-light peers by 2024.

The research also reveals that insurance-integrated firms display higher equity betas and negative sensitivity to rising interest rates, fundamentally altering their risk profile.

Industry-Wide Implications

The concentration of growth among insurance-integrated firms has profound implications for the broader financial services industry, according to the report.

With insurance-backed AAMs now controlling 35% of new U.S. fixed and fixed-indexed annuity sales (up from 7% in 2011), traditional boundaries between asset management and insurance have effectively dissolved.

"The shift from episodic fundraising to continuous, liability-backed capital re-engineers both the funding cycle and the risk-return profile of leading sponsors," the researchers observe.

This transformation also enables firms to pursue capital-intensive strategies previously considered "subscale or uneconomic", while creating cross-platform origination synergies that further entrench competitive advantages.

The scramble also comes as private credit has become central theme for life reinsurance portfolios in the hunt for higher yields amid stable but elevated interest rates.

However, the Harvard study suggests several critical questions remain.

"First, to what extent will capital allocation favor one revenue stream over another—spread versus fee—especially in downturns," the report states. "Second, how will regulatory responses (e.g., higher capital charges on privately originated assets) affect the scalability of the model? Third, what are the implications for policyholders, institutional LPs, and financial stability as traditional boundaries between asset management and insurance continue to blur?"

- Cat Models, Insurers Should Expect Additional "Nature-Based" Risk Mandates

Catastrophe modelers and insurers face a new regulatory reality as states increasingly mandate the integration of nature-based risk metrics—from wetland flood absorption to forest fire management—into pricing models.

Deep Divisions Will Likely Continue Over California's Wildfire Insurance Crisis As Models Finally Become Reality

Stark disagreements about the health of California's insurance industry and the need for government intervention emerged during a high-level forum examining the state's wildfire insurance crisis.