As President-elect Donald Trump announces senior staff appointments and accelerates his transition to prepare for the January 20 inauguration, the insurance industry might not have to wait over two months to see how it will be impacted by the new administration.

Funding for the National Flood Insurance Program (NFIP), often criticized by conservative lawmakers and policy analysts, is set to expire on December 20 this year. This deadline will provide an early test of the Republican commitment to reduce costly federal programs deemed “unsustainable.”

If not renewed during the lame-duck session of Congress, the NFIP’s borrowing authority from the U.S. Treasury will shrink from $30.425 billion to just $1 billion. Without this funding, the federal government would lose the ability to issue new flood insurance policies. However, policies entered into before the expiration would remain valid until their one-year term ends, according to the Congressional Budget Office (CBO).

The first shots in the pre-Trump administration debate over the NFIP’s future have already been fired. The libertarian think tank Cato Institute argued yesterday that federal flood insurance should transition to the private sector as soon as possible.

“One key reform is transitioning to a fully private flood insurance market, coupled with targeted, means-tested subsidies,” Cato stated. “Allowing the market to set risk-based premiums would better align costs with actual risks, incentivize safer development, and minimize taxpayer burdens.” Moving to a private market, the institute argues, would also promote responsible development and improve risk assessment.

Project 2025, a reform agenda backed by the Heritage Foundation, has similarly prioritized the NFIP as a target in a potential second Trump administration.

“[Subsidies] and bailouts only encourage more development in flood zones, increasing potential losses to both NFIP and the taxpayer,” the report says. “The NFIP should be wound down and replaced with private insurance, beginning with the least risky areas currently covered by the program.”

In a proactive move ahead of the NFIP’s funding battle, the Federal Emergency Management Agency (FEMA) issued a press release last week stating that over 72,000 NFIP policyholders had filed flood damage claims after this year’s Hurricanes Debby, Helene, and Milton. These policyholders have received approximately $894 million to repair their properties and replace contents.

FEMA followed up yesterday, noting that Hurricane Helene alone could result in NFIP losses estimated between $3.5 billion and $7 billion.

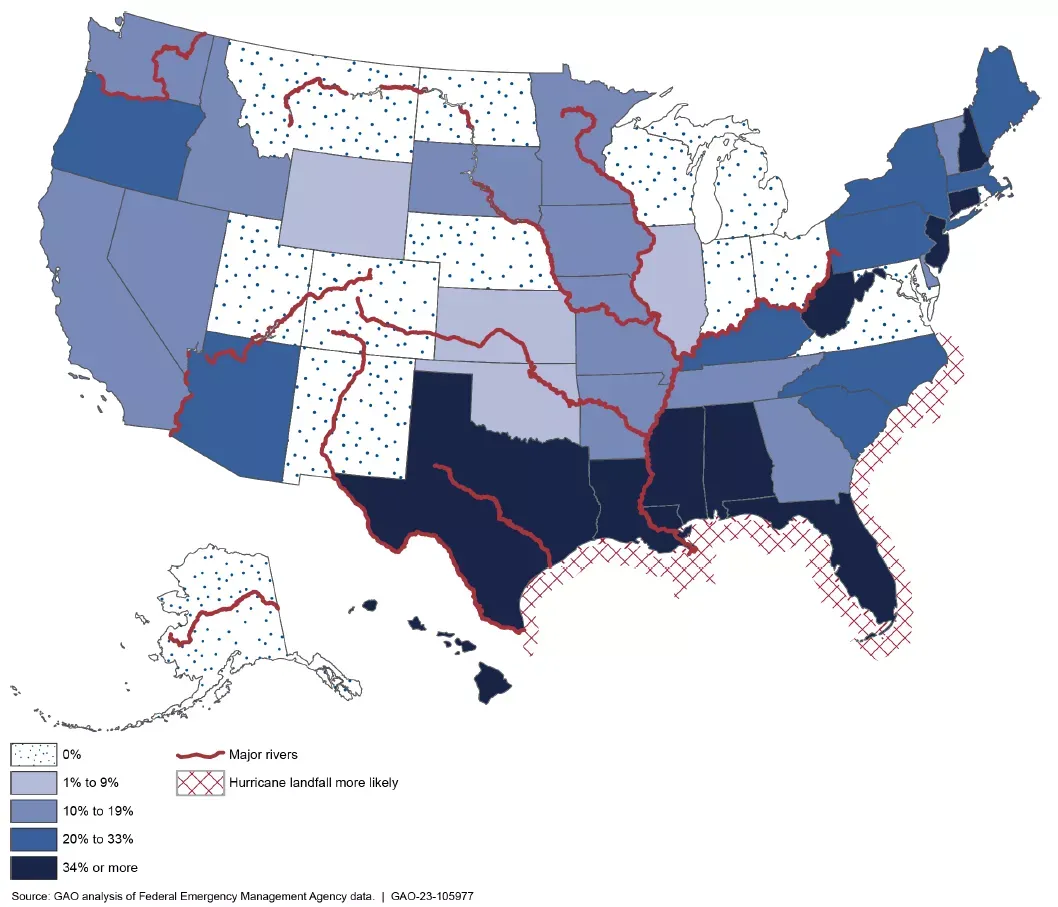

Indeed, we found the current approach is expected to double rates over time for the average policy. Homeowners in five Gulf Coast states—Alabama, Florida, Louisiana, Mississippi, and Texas—are among those expected to see the largest increases because rates in those states had been previously among the most underpriced.