Thanks for previously subscribing to the Risk Market News newsletter. We have restarted publishing and switched email platforms. We are also changing to a paid subscription model in 2020, but as a thank your for your earlier interest we will continue sending you the subscriber-only newsletter through January 1.

Texas Deals With Rate Pushback, Reinsurance Pricing and Modeled Loss Challenge

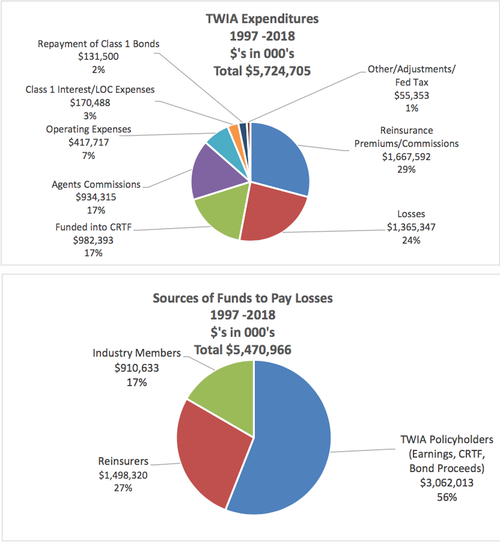

The Texas Windstorm Insurance Association (TWIA) is proposing an increase in its reinsurance spend as the state-backed insurer deals with public pushback regarding a proposed rate increase and new legislation that requires it to tie reinsurance purchases to a one-in-100 probable maximum loss.

According materials of meeting today, TWIA is proposing:

- Reinsurance costs are projected to equal $93.1 million in 2020 based on a projected attachment point of $2.22 billion and a total limit purchased of $1.88 billion, compared to $90.2 million in 2019.

- Aggregate reinsurance purchased is proposed to be reduced from $2.1 billion to $1.88 billion “based on declining exposure and an increase in the Catastrophe Reserve Trust Fund.

- Ceded premium is projected to increase based on an assumed increase in the rate on line (premium/limit) from 4.3% to 4.95% for the overall program.

- Net Earned Premium is budgeted to decline to $262.9 million in 2020, down $26.8 million (9.2%) from the $289.7 million projected earned premium in 2019. That is based on the projected decline in written premium, the impact of ceded reinsurance costs and the depopulation program.

At the same time, TWIA continues to wrestle with implementation of new legislation that puts preconditions on reinsurance purchases through a modeled PML:

- Determine a one-in-100-year probable maximum loss annually.

- Disclose to the PML publicly, along with the method used to determine it.

- Determine the amount of reinsurance premium applicable to the reinsurance coverage that exceeds its one-in-100-year probable maximum loss and disclose the amount of reinsurance premium.

U.S. Report Pushes Private Market Data, Finance Structures

The U.S. government is trumpeting its efforts to push more insured risks into the private market through the use of new technologies and finance structures. In its 2019 National Preparedness Report released last week, the U.S. Department of Homeland Security said that insurers are expanding “data collection, data analytics, and geospatial analysis” to price risks more accurately and expand their market share in traditionally publicly-backed insurance markets.

With improved data, insurers can recognize property- specific risk differences within previously broad geographic areas. Some insurers are making clearer linkages between pre-disaster mitigation activities and premiums for disaster recovery insurance.

The report also promoted the Federal Emergency Management Agency’s (FEMA) multi-year efforts to place more flood risk into the private market the the National Flood Insurance Program (NFIP). The report stated that the NFIP’s Reinsurance Program allowed FEMA to use 28 insurance companies to secure $1.46 billion in reinsurance coverage for flood loss and transfer $500 million in financial risk to capital markets in 2018.

In addition, the report also argued that local governments will take up additional catastrophe bond coverage to increase private market participation in traditionally publicly-backed risks.

Between 2010 and 2017, the cost of issued catastrophe bonds more than doubled across the United States (2018 data are not yet available). The increasing use of catastrophe bonds is another way that insurance providers are utilizing this market opportunity while helping communities ensure the availability of resources needed to help individuals, communities, and businesses recover from major disasters.

Floodplain Purchase Have Better ROI Than Development

Purchasing flood prone property, and then conserving land from development may be a better cost benefit to the U.S. than allowing development and mitigating or insuring the risk from loss, according to a new study.

The study, conducted by modeling firm Fathom and researchers from the University of Bristol in the UK, found that the cumulative avoided future flood damages exceed the costs of land acquisition for more than one-third of the unprotected natural lands in the 100-yr floodplain.

Large areas have an even higher benefit–cost ratio: for 54,433 km2 of floodplain, avoided damages exceed land acquisition costs by a factor of at least five to one. Strategic conservation of floodplains would avoid unnecessarily increasing the economic and human costs of flooding while simultaneously providing multiple ecosystem services.

The report adds that part of the cause of the inability of public or private markets to accurately measure the flood risk was the poor state of flood mapping in the U.S. The report states that “incomplete and inaccurate mapping” prevents planners and governments to focus development to limit exposure and mitigate flood risk.

[Nearly] 40% of the conterminous United States [lacks] this mapping for riverine floodplains, limiting the potential to plan new development to minimize future fluvial flood risk. Recent research has highlighted the shortcomings of current information and used new comprehensive floodplain mapping, revising estimates of people at risk from a 100-yr flood from 13 million to more than 40 million